- The Unsophisticated Investor

- Posts

- The Role of Syndicates in Modern Startup Investing

The Role of Syndicates in Modern Startup Investing

Scott Ashmore & Rob Halligan

February 04, 2026

Hello friends, and welcome to The Unsophisticated Investor! Brought to you by Scott & Rob, the founders of Shuttle!

If you want to invest alongside the VC funds who've backed breakout companies like Revolut, Asana, JustEat, Bolt, Lets Get Checked, Loom, Runna, Charlotte Tilbury, Deel, Aircall, AngelList, Carta, TransferWise and many more, regardless of your knowledge, network or net worth, join our limited waitlist now.

Now, let’s get into it 👇

Why syndicates exist at all

Early-stage investing has never been a clean market. There is no exchange, no continuous pricing, and no single source of capital. Instead, founders raise money one conversation at a time, often from individuals with different motivations, time horizons, and levels of experience.

Syndicates emerged as a practical response to that fragmentation. They are not a new asset class, nor a shortcut to better returns. They are a coordination mechanism - a way to organise capital, decision-making, and accountability in an environment that would otherwise remain highly inefficient.

In practice, syndicates exist to reduce friction. For founders. For investors. And for the system that sits between them.

What a syndicate actually is

At its simplest, a syndicate is a way to pool individual investors into a single investing entity.

Rather than a company raising capital from dozens of separate shareholders, a syndicate groups those investors together under one structure. From the founder’s perspective, that group appears as a single line on the cap table. From the investor’s perspective, it provides access to a deal they might not otherwise see or be able to participate in efficiently.

A typical syndicate is led by one investor who sources the opportunity, negotiates the terms, and commits their own capital. Other investors then choose whether to participate alongside them, investing on the same economic terms.

The structure does not change the fundamentals of the investment. The company is still early-stage. The risks are unchanged. Liquidity remains limited. What the syndicate changes is organisation - how capital enters the company, and how responsibility is distributed among the people backing it.

The lead investor’s role

Every syndicate is shaped by its lead investor. The structure may pool capital, but judgment remains concentrated.

The lead is responsible for sourcing the opportunity, assessing the company, and deciding whether it merits backing at a given valuation. They typically negotiate terms directly with the founder and set the parameters under which others can participate.

This role carries both influence and obligation. While other investors rely on the lead’s access and experience, the lead also commits their own capital and reputation to the deal. Their incentives are aligned with the group, but their decisions have an outsized impact.

In practice, the quality of a syndicate is less about the platform it sits on and more about the discipline of the person leading it. Structure can organise capital, but it cannot substitute for sound judgment.

How syndicates change access - carefully

For most of the last few decades, access to early-stage deals has been driven by proximity. You invested because you knew the founder, worked in the same network, or were already part of an established investor circle.

Syndicates formalise that process. They turn informal access into a repeatable structure, allowing more investors to participate without expanding the founder’s workload or fragmenting ownership. In that sense, syndicates widen the top of the funnel.

What they do not do is reduce risk. The underlying characteristics of early-stage investing remain intact: limited information, long time horizons, and a high probability of loss. A syndicate can improve access and organisation, but it cannot change the fundamental economics of backing young companies.

The distinction matters. Better access should be understood as improved participation, not improved outcomes.

The trade-offs that syndicates introduce

Syndicates solve coordination problems, but they also introduce new dynamics that investors need to understand.

Decision-making becomes delegated. Participants rely on the lead investor not only for sourcing and diligence, but also for judgment calls that may evolve over time - follow-on participation, signalling in future rounds, or responses to underperformance. That reliance is structural, not incidental.

Information flow also changes. While syndicates can improve consistency of communication, they can also create distance. Updates are filtered. Context is summarised. Investors gain efficiency, but lose direct proximity to the company.

None of this is inherently negative. It is the price of organisation. The mistake is assuming syndicates remove complexity. In reality, they redistribute it - away from logistics and toward trust in the lead.

Understanding that trade-off is central to using syndicates responsibly.

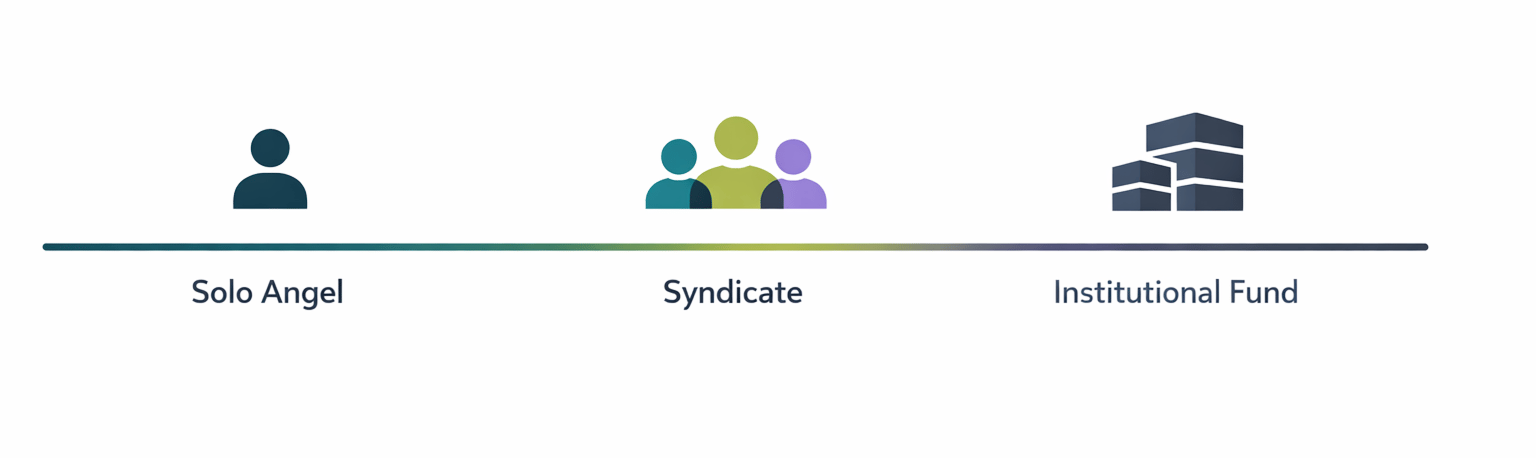

Where syndicates sit in the investment landscape

Syndicates are often discussed in isolation. In practice, they sit between two established models.

At one end are institutional funds. They offer diversification, formal governance, and a clear mandate, but operate on fixed timelines and are inaccessible to most individuals. Decisions are committee-driven, and investors trade discretion for scale.

At the other end are solo angels. They invest directly, retain full control, and stay close to founders, but are constrained by personal capital, time, and access. Concentration risk is unavoidable.

Syndicates occupy the middle ground. They retain the flexibility of individual decision-making while introducing structure and scale. Capital moves faster than in funds, but with more organisation than solo investing.

This positioning explains their growing relevance. Syndicates are not replacing funds or angels. They exist because the space between those models needed a workable structure.

Where syndicates break down

The effectiveness of a syndicate is highly uneven. The structure itself is neutral. Outcomes depend on how it is used.

Lead quality varies. Some leads bring deep domain knowledge, disciplined pricing, and long-term engagement. Others offer little more than access. For participants, the difference is difficult to see upfront but decisive over time.

Incentives can also misalign. Fee structures may reward deal volume over selectivity. Social dynamics can discourage critical challenge. In weaker syndicates, momentum replaces analysis.

Finally, governance remains limited. Syndicates rarely exert the influence or oversight of institutional funds. When companies underperform, options narrow quickly.

These limitations do not invalidate the model. They define its boundaries. Syndicates work best when investors treat them as a structured extension of individual judgment - not a substitute for it.

Why syndicates matter more now

The relevance of syndicates has increased not because early-stage investing has changed, but because the surrounding system has.

Companies are staying private for longer. More value is created before any public listing, and participation in that phase has historically been limited to a narrow set of investors. Syndicates provide a way to organise individual capital around that extended private phase.

At the same time, professional investors outside traditional venture circles are looking for structured exposure earlier in a company’s life. Regulation and platform infrastructure have reduced coordination and compliance friction, making repeat participation possible without informal networks.

Syndicates sit at the intersection of these shifts. They adapt an old practice - individuals backing founders - to a market where scale, oversight, and repeatability now matter.

Their growing role reflects a change in capital formation, not a change in risk.

What this means for modern investors

Syndicates change how early-stage investing is accessed, not what it indicates or guarantees.

Judgment moves upstream. The quality of the lead, their incentives, and their discipline become central variables. Evaluating those factors matters more than evaluating individual deals in isolation.

Portfolio construction still applies. Outcomes remain skewed. Losses are common. Time horizons are long. Syndicates do not alter those dynamics - they simply provide a different way to participate within them.

For investors, the implication is structural awareness. Understanding how capital is organised, where decisions are made, and what trade-offs are accepted is part of managing exposure in private markets.

Access is easier. Responsibility is unchanged.

Syndicates as infrastructure

Syndicates do not change how startups succeed or fail. Product-market fit, execution, timing, and capital discipline still determine outcomes.

What syndicates change is organisation. They shape how capital is gathered, how responsibility is concentrated, and how individuals participate in an otherwise fragmented market.

In modern startup investing, structure matters. Not because it improves results, but because it defines who is involved, how decisions are made, and where accountability sits.

Syndicates are not an edge. They are infrastructure.

What we’ve been working on at Shuttle

Speaking of Syndicates… Shuttle deploy is live and ready to demo 🚀

Planning some exciting partnerships for 2026 and beyond 🧑🤝🧑

Making preparations for Drop No.5 ⌛️

Fipto Becomes Europe’s First Dual-licenced Stablecoin Payment Institution with New MiCA LicenceFipto, the leading regulated payment infrastructure for stablecoins, today announced it has been granted the Crypto-Asset Service Provider (CASP) licence by the French Autorité des Marchés Financiers (AMF). | Spain announces plans to ban social media for under-16sThe ban, which still needs parliamentary approval, is part of a raft of changes that include making company executives responsible for "illegal or harmful content" on their platforms. |

The Unsophisticated Investor is brought to you by Scott & Rob, the founders of Shuttle. We’re both sick of private markets being a playground exclusive to the ultra-wealthy so we started a company to challenge the status-quo. Shuttle’s singular focus is to unlock private markets for Millennial and Gen Z tech professionals and help them build wealth through the highest performing private market opportunities.

Scott & Rob

Shuttle Co-Founders